QUESTION TO CLAUDE 3: The EU and China lag behind the US in economic dynamism, measured by start-up activity, number of unicorns, age of unicorns (younger indicates more rapid innovation), and in productivity growth. Can you document this and tell me why?

ANSWER: Here is the data to document the economic dynamism gap between the US, EU, and China, along with some key reasons behind it:

Start-up Activity:

- The US had over 63,000 startups in 2020, compared to around 37,000 in the EU and 25,000 in China. The US accounted for over 50% of global venture capital investment.

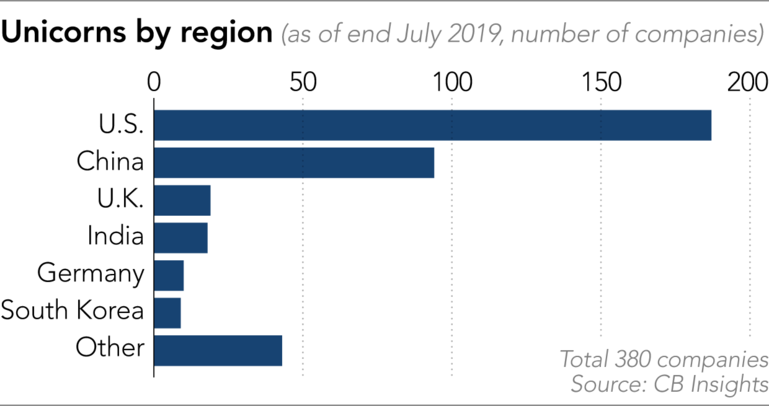

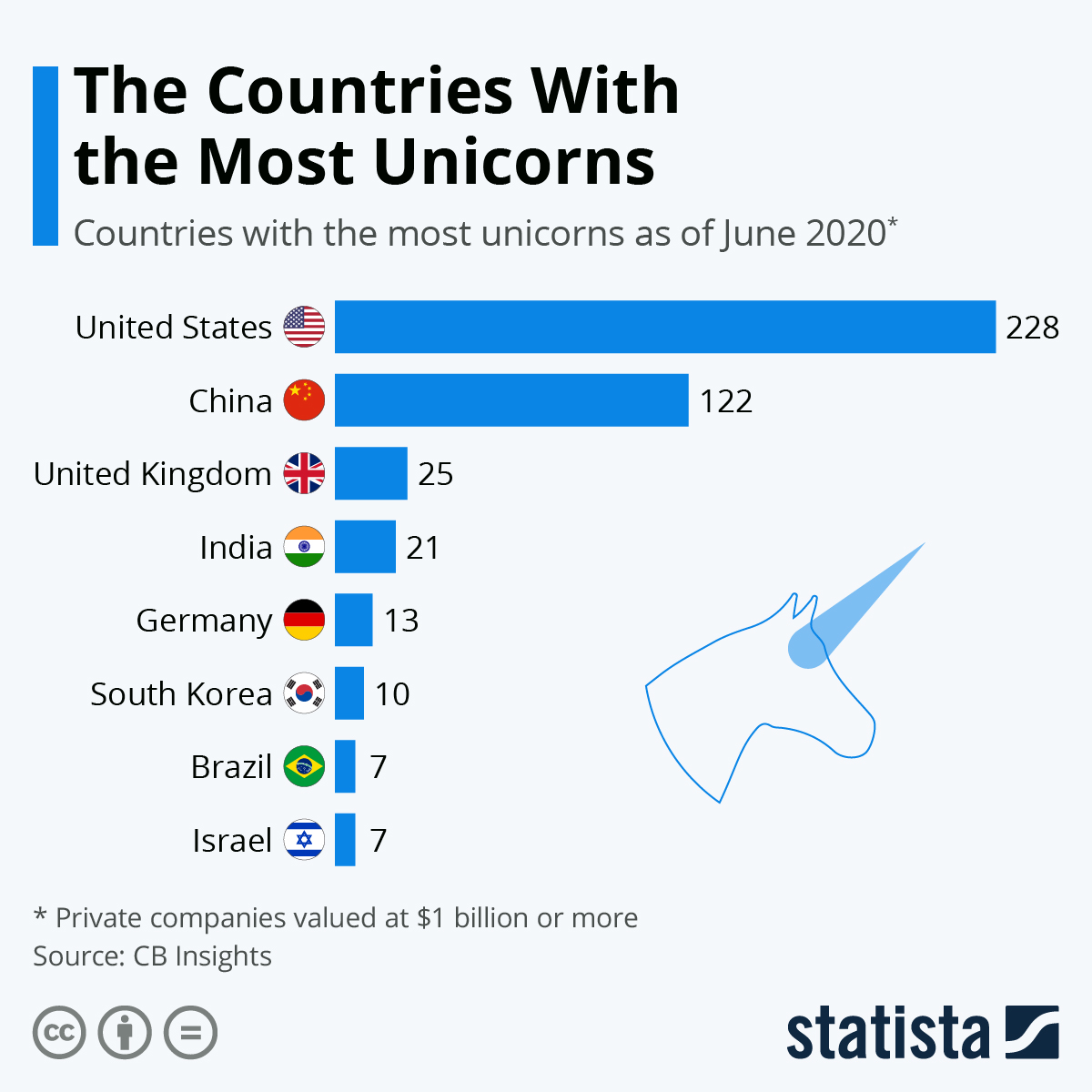

Unicorns (private companies valued at $1B+):

- As of 2023, the US has 704 unicorns, China has 258, and the EU has 139. The total value of US unicorns is $2.4 trillion vs. $862 billion for China and $449 billion for the EU.

- The US represents 51% of the world's unicorns by number and 65% by valuation. China and the EU lag significantly behind.

Age of Unicorns:

- The median age of US unicorns is 7 years vs. 9 years for Chinese unicorns, indicating more recent startup success in the US. [Claude 3 unable to find data on EU unicorns]

Productivity Growth (average annual labor productivity growth 2010-2019):

- US: 1.0%

- EU: 0.7%

- China: 7.1% (but from a much lower base)

Key Reasons for the US Lead:

- Larger, more developed venture capital and private equity industry in the US fueling more startup investment. US VC deal value was 5-7X higher than China and the EU in recent years.

- US equity markets provide better exit opportunities for startups via IPOs. US represented over 60% of global IPO proceeds in 2021.

- Huge US domestic market enables startups to scale quickly. EU is fragmented across countries and China's market is difficult for foreign firms.

- Top US universities and companies attract global talent. Over 50% of US unicorn founders are immigrants.

- Historically strong intellectual property protections, rule of law, and business-friendly regulations in the US encourage innovation and risk-taking.

- Deeply rooted culture of entrepreneurship and risk-taking in the US compared to more risk-averse cultures in the EU and China's state-led system.

While China leads on productivity growth, this is largely due to catch-up growth from a low base. On most measures of economic dynamism, especially in the innovation economy, the US maintains a substantial lead over the EU and China as of 2023. But the gap has been narrowing over time.

Economist: America is in the midst of an extraordinary startup boom

{kind=link}

{kind=link}