Sunday, October 30, 2016

How information moves markets: Hilary futures crash

Friday, October 28, 2016

Cross your fingers: Nashville's risky pension portfolio

In the past, when Nashville's pension fund earned more than required to fund the pensions, the politicians spent the surplus; but when it came up short, they did not fund the difference. This lead to systematic underfunding. Then the State passed a law to force Nashville and Memphis to fund their pensions.

Now, we learn that Nashville is investing in risky assets to reach its targeted 7.5% return:

So how is it doing?

Keep your fingers crossed!

HT: Preston

Now, we learn that Nashville is investing in risky assets to reach its targeted 7.5% return:

Since the 2008 financial crisis, Nashville’s pension managers have been shifting taxpayer money into junk bonds, hedge funds, troubled mortgages, private equity funds and other alternatives to conservative stocks and bonds. If successful, these “alternative investments” can earn greater profits, but they also demand high fees and carry the risk of heavy losses.

So how is it doing?

Nashville's investments have shown mixed results. After taking out fees, the city’s fund grew by 4.7 percent a year since 2008, on average, while the Standard & Poors 500 gained 6.6 percent.

Keep your fingers crossed!

HT: Preston

Thursday, October 27, 2016

Coal comeback

In the graph above, we see a slight increase in quantity, which represents a dramatic change form the downward trend in demand. As a result, railroad stocks are up as railroads and barges are the only way to move coal.

HT: FT

Before you answer, make sure you understand the question!

Take the following quiz:

1. A bat and a ball cost $1.10 in total. The bat costs $1.00 more than the ball. How much does the ball cost? ____cents

2. If it takes 5 machines 5 minutes to make 5 widgets, how long would it take 100 machines to make 100 widgets? _____minutes

3. In a lake, there is a patch of lily pads. Every day, the patch doubles in size. If it takes 48 days for the patch to cover the entire lake, how long would it take for the patch to cover half of the lake? _____days

Each of these questions has an obvious answer that is wrong. However, if you take one minute to think about the questions--BEFORE YOU ANSWER--you will come to the correct, less obvious answer. Over the years, I have found that those who can answer these questions tend to do very well in my economics classes.

MORAL: before answering the question, spend a minute or two thinking about what the question is.

=================ANSWERS=================

Question 1: Though the quick intuitive answer is 10 cents, a moment's reflection leads to the realization that 10 cents is not a full dollar less than $1.00. (If you're sleepy: 10 cents is 90 cents less than $1.00.) The accurate solution can be reached through a little 8th grade algebra:

If the cost of the ball is x, the cost of the bat is x + 1.

x + (x+1) = 1.10

2x +1 = 1.10

2x = 0.10

x = 0.05, or 5 cents

Answer: the ball costs 5 cents and the bat costs $1.05, for a total of $1.10.

Question 2: Your brain screams at you that the answer must be 100, because your intuitive side sees the 5-5-5 pattern in the first example, and 100-100-100 just looks right. But if it takes 5 minutes for 5 machines to make 5 widgets, it doesn't take 20 times as long for 20 times as many machines to make 20 times the widgets. It will take the same 5 minutes for 100 machines to make 100 widgets, and it will take 5 minutes for 1000 machines to make 1000 widgets, and so on, because each machine spits out one widget every five minutes. That is the rate of widget production for the machines, and it doesn't change no matter how many machines you are running at once.

Answer: it would take 5 minutes for 100 machines to make 100 widgets.

Question 3: This trick here is that the lily pads grow at an exponential rate, not an arithmetic rate. On the day before the 48th day, the pond was only half-covered in lily pads; the day before that, one-quarter covered; the day before that, one-eighth covered; the day before that, one-sixteenth covered. Go back two weeks from the 48th day (day 34) and you will be hard-pressed to find any lily pads on the lake. It will be only 1/16,384 covered on that day. This means only .006% of the surface will be covered by a lily pad. Imagine how powerful a microscope you'd need to detect any lily paddage at all on day 1.

Answer: the pond will be half-covered in lily pads on the 47th day.

HT: Big Thinking

Saturday, October 22, 2016

How do you estimate the competitive effects of hospital mergers?

The answer in a report by two middling economists:

In the graph above, the two merging hospital systems are denoted by red and blue, while the non merging firms are denoted in yellow. The circles are centered on zip codes and denote the number of patients who go to each hostpital system. Using these data, the economists estimated a "gravity choice" model that showed

- ... the merged hospitals are each other’s closest competitors. If Wellmont were to close, 75 percent of its patients would go to a Mountain States hospital. Similarly, if Mountain States were to close, 72 percent of its patients would go to a Wellmont facility.

These data are used to determine how much price would rise following the merger.

Follow the Merger's progress through the regulatory process at the Johnson City Press. UPDATE: the parties realized that the report would have lead the FTC to challenge the merger (and likely win) so the parties asked the state legislatures of VA and TN to regulate the merger so they could reduce costs (by closing competing hospitals) without the risk to consumers of rising prices. Presumably the state regulation would keep prices low in lieu of competition between the two systems.

Follow the Merger's progress through the regulatory process at the Johnson City Press. UPDATE: the parties realized that the report would have lead the FTC to challenge the merger (and likely win) so the parties asked the state legislatures of VA and TN to regulate the merger so they could reduce costs (by closing competing hospitals) without the risk to consumers of rising prices. Presumably the state regulation would keep prices low in lieu of competition between the two systems.

Friday, October 21, 2016

Thursday, October 20, 2016

When do managers care about their competitors' profitability?

When stocks are commonly owned by big institutional shareholders, these big shareholders reward managers for industry performance, rather than individual company performance, as that maximizes the value of their portfolio:

See our earlier blog post on How to decrease industry rivalry.

... in industries with high common ownership, top managers receive almost twice as much pay for the good performance of their competitors as managers do in industries with low common ownership. This effect is even more pronounced for CEOs alone. Essentially, CEOs are rewarded more for the good performance of their competitors than they are for the performance of the company they run.

See our earlier blog post on How to decrease industry rivalry.

Wednesday, October 19, 2016

Texas Physicians Threatened by TeleMedicine

It seems that the Texas Medical Board had tried to keep

patient care via the Internet from competing with traditional medicine. As

reported by the Texas

Standard, they required physicians to meet with patients in person before

they were allowed to treat them remotely. Since 35 rural Texas counties have no physicians at all, this regulatory entry barrier all but kills the main

benefit of telemedicine. Even in urban areas, telemedicine would likely

generate serious competition to traditional health care providers.

This requirement primarily affected Teladoc, a company based here in North Texas. But Teledoc sued that the requirement violated antitrust laws and won in lower court. The Texas Medical Board appealed but recently dropped their appeal, perhaps because Teledoc was backed up by the FTC and DOJ. Since the Texas Medical Board is made up of incumbent physicians, this is not unlike the teeth whitening case in North Carolina.

This requirement primarily affected Teladoc, a company based here in North Texas. But Teledoc sued that the requirement violated antitrust laws and won in lower court. The Texas Medical Board appealed but recently dropped their appeal, perhaps because Teledoc was backed up by the FTC and DOJ. Since the Texas Medical Board is made up of incumbent physicians, this is not unlike the teeth whitening case in North Carolina.

REPOST: sunk-cost fallacy in real estate

Tuesday, August 24, 2010

Sunk-cost fallacy in real estate

In the post below this one, we show that the housing market can have excess supply. This post shows that it is due to thereluctance of homeowners to sell at a loss, a version of the sunk cost fallacy.

Two homeowners, with identical houses, will list the houses at different prices, depending on what they paid for the house because of what psychologists call "loss aversion." Unfortunately for these loss-averse sellers, buyers don't suffer from similar delusions,

Two homeowners, with identical houses, will list the houses at different prices, depending on what they paid for the house because of what psychologists call "loss aversion." Unfortunately for these loss-averse sellers, buyers don't suffer from similar delusions,

Properties listed above the market price just sat there. In the Boston market over all, sellers listed their properties for an average of 35 percent above the expected sale price, and less than 30 percent of the properties sold in fewer than 180 days. In other words, much of the market went into a deep freeze as many people held out for market prices that no one would reasonably pay.

Note that this reluctance is similar to the reluctance of businesses to pull the plug.

Tuesday, October 18, 2016

Does zoning causes inequality?

It used to be that there were two ways to make more money: invest in your human capital (education) or move to a richer state. WSJ article on how housing has reduced the profitability of the second mechanism:

Moving to a wealthier area in search of job opportunities has historically been a way to promote economic equality, allowing workers to pursue higher-paying jobs elsewhere. But those wage gains lose their appeal if they are eaten up by higher housing costs. The result: More people stay put and lose out on potential higher incomes.Land use restrictions are behind the increase in price

The developed residential area in Atlanta, for example, grew by 208% from 1980 to 2010 and real home values grew by 14%. In contrast, in the San Francisco-San Jose area, developed residential land grew by just 30%, while homes values grew by 188%.

Wednesday, October 12, 2016

Tying stock pickers' pay to performance

Steven Cohen is changing how he evaluates and rewards his stock pickers:

By doing this, he hopes to attract better pickers to his firm (adverse selection). Note that he is measuring excess returns adjusted for the riskiness of the portfolio, i.e., alpha.

Note the link to yesterday's post about how best to tie pay to performance. By using alpha (risk adjusted return), instead of raw return, Cohen is practicing the "informativeness principle," measuring performance using all information about productivity, including information about risk.

Point72 had been paying its stock pickers a fixed 20% bonus on investment returns regardless of how they performed against broader benchmarks. That meant they could be paid handsomely just for matching a rising market.

Under the new bonus system, Point72 will boost those payouts to as much as 25%, but it will only pay the top bonuses on so-called alpha, industry parlance that roughly translates to investment performance above a market benchmark.

By doing this, he hopes to attract better pickers to his firm (adverse selection). Note that he is measuring excess returns adjusted for the riskiness of the portfolio, i.e., alpha.

Note the link to yesterday's post about how best to tie pay to performance. By using alpha (risk adjusted return), instead of raw return, Cohen is practicing the "informativeness principle," measuring performance using all information about productivity, including information about risk.

Sterling devaluation and banks

Foreign banks with big servicing centres in the UK — such as Citi’s centre of excellence in Belfast — gain because they pay for those centres in sterling, and they receive more sterling for their home currency when the pound is weak.

LOSERS:

The flip side of the cost benefit is that every pound in profit banks earn in the UK is worth less when they repatriate it to their home currencies. US banks generally run their profitable European trading and investment banking businesses from London so the sterling devaluation is a “a drag on revenues from the UK and on pre-tax margins”, according to Brian Kleinhanzl, a New York-based analyst for KBW.

Tuesday, October 11, 2016

Luxury goods and the sterling devaluation

The sterling devaluation is helping British exporters and hurting British consumers. However, it is also helping British Tourists:

Since Britain voted in June to leave the European Union, sterling has tumbled 17% as of Friday’s close, having set fresh three-decade lows last week. The fall has ratcheted up prices here of imported wine, electronics and even some cars. But most luxury-goods makers—protected by typically fat margins for their products—haven’t yet raised their prices. That has suddenly made the U.K. the least expensive market in the world for a bevy of luxury goods, according to analysts.

HT: Adam

Sunday, October 9, 2016

Why are trailer parks such good investments?

The very government restrictions that have created the affordable housing crisis, offer an opportunity to investors in trailer parks:

Franke Rolfe, a Stanford graduate who teaches people how to profit in the mobile home industry, buys dilapidated trailer parks, cleans them up, and rents mobile homes to the working poor. A 2014 New York Times Magazine article reported that he and a partner earned a 25% return on their investment.

Trailer parks’ appeal to these investors is simple. Millions of Americans struggle with rent payments, but still want a lawn. For them, mobile homes are the cheapest form of housing available. At the same time, it’s rare for someone to build a new mobile home park, because no homeowner wants a trailer park nearby. An industry with healthy demand but a fixed supply attracts the country’s capitalists.HT: MarginalRevolution.com

Can the government bring stability to markets?

According to Alan Greenspan's new biographer, not without moral hazard:

If the Fed responds when markets turn down but doesn’t suppress exuberance when markets are up, private actors will have an incentive to take on more risk than they otherwise would. This can undermine natural market discipline. Mr. Mallaby believes that in his responses to negative shocks, Mr. Greenspan crossed the line from being the “guru”—“the man who knew”—to becoming the “guardian angel.”

BOTTOM LINE:

“The delusion that statesmen can perform the impossible—that they really can qualify for the title of ‘maestro’—breeds complacency among citizens and hubris among leaders.”

Saturday, October 8, 2016

Is the pound depreciation good for Britain?

The FT has the answer:

Of course, as many will point out, a decline in the currency is good for exporters. It is also good for the foreign currency earnings of the multinationals listed in the FTSE 100. But unless a currency is overvalued (as the pound was in 1992), it is folly for a nation to celebrate a sharp decline. If devaluation were the answer to economic success, people in Venezuela and Zimbabwe would be rich. A weaker currency is a decline in the terms of trade; it costs more for citizens to buy foreign imports they want and their exports are lower in price. As a trading nation with a current-account deficit, Britain is dependent on the kindness of strangers; the willingness of foreign investors to send capital.

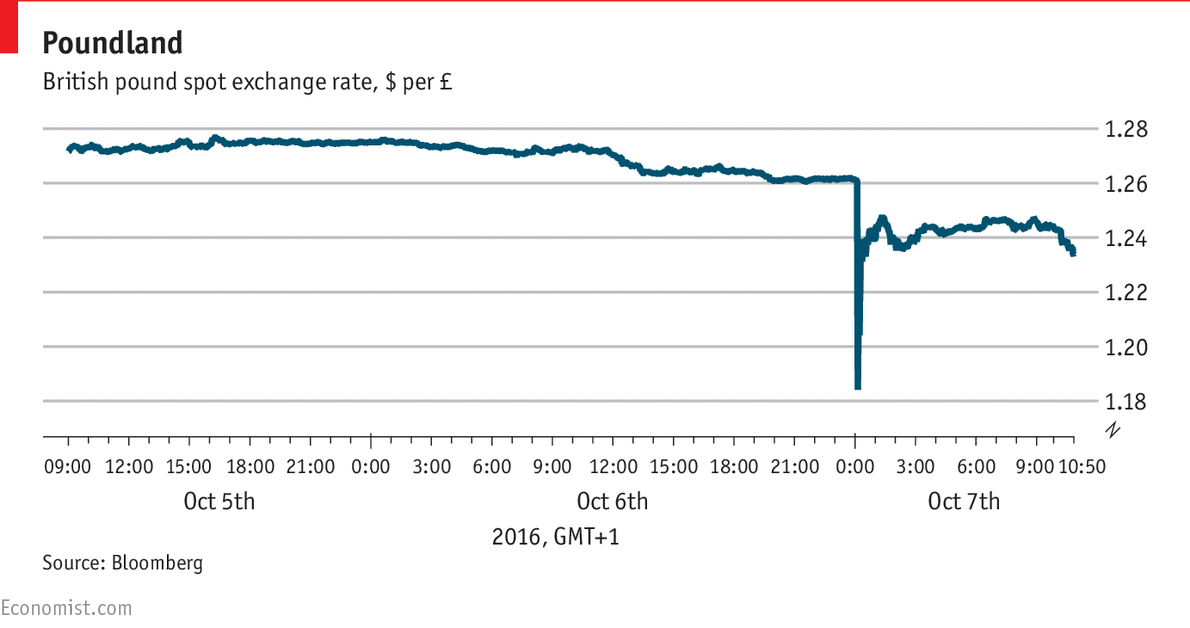

Friday, October 7, 2016

Never start a land (or price) war in Asia

Who will outlast whom, Flipkart vs. Snapdeal?

Both signed deals with big financial partners, Wal-mart and Amazon, trying to drive each other out of e-business in India. How long until they realize that this kind of predation rarely pays? If they don't, investors may want to step in a stop it before they lose too much money.

Until Wal-mart and Amazon get tired to losing money, keep shopping.

HT: Brian

Both signed deals with big financial partners, Wal-mart and Amazon, trying to drive each other out of e-business in India. How long until they realize that this kind of predation rarely pays? If they don't, investors may want to step in a stop it before they lose too much money.

At some point, if Amazon believes that the price of a scorched earth battle is too high, it might sue for peace and move to merge with Flipkart. If that happens, both parties will win.

Until Wal-mart and Amazon get tired to losing money, keep shopping.

... as consumers, you would be well-advised to make the best of the big sales being run by online retailers. The sale will last only till the money lasts.

HT: Brian

Wednesday, October 5, 2016

Did the government cause the affordable housing crisis?

"Yes," says the Washington Post, for three reasons:

1. Restrictive zoning reduces the profitability and therefore the supply of housing:

2. Regulatory delays and requirements raise costs to the point where only high-end apartments are profitable (Nashville's problem):

3. FHA loans prohibit mixed use, further reducing the profitability and supply of housing:

1. Restrictive zoning reduces the profitability and therefore the supply of housing:

The White House’s calls for local policymakers to expand by-right development (where allowable building projects can proceed administratively, without years-long public hearing processes) and accessory dwelling units, to repeal or reduce minimum parking requirements, and to rezone neighborhoods for greater possible density all amount to restoring landowners’ rights to develop property as they and the market see fit. As the tool kit notes, inappropriate parking requirements, in particular, can raise the expected rent in a new development by as much as 50 percent, while depriving towns of socially and commercially productive land.

2. Regulatory delays and requirements raise costs to the point where only high-end apartments are profitable (Nashville's problem):

Establishing by-right development and streamlining local permitting processes will allow developers to respond nimbly to market demands and will relieve the “guilty until proven innocent” status of new building development, which depresses construction starts across the country by delaying and inhibiting housing projects. What’s more, adopting leaner codes would remove obstacles to the countless smaller developers and would-be builders who want to invest in strengthening their local communities, but currently can’t afford to navigate the vast regulatory burdens and uncertain futures awaiting anyone who tries to build in America today. Trulia economist Ralph McLaughlin found that these regulatory delays may have an even bigger impact on housing production than zoning restrictions.

3. FHA loans prohibit mixed use, further reducing the profitability and supply of housing:

To this day, FHA standards for loans, which set the market for the entire private banking sector, prohibit any but the most minimal commercial property from being included in residential development. As a groundbreaking report by New York City’s Regional Plan Association found, these standards are “effectively disallowing most buildings with six stories or less.” And depending on the program, a building could have to reach to 17 stories before it is eligible for participation in the normal housing markets. Without the FHA’s blessing, projects are granted the “nonconforming” kiss of death unless their developers can persuade a local bank to write an entirely customized loan for them, one whose risk the bank would have to keep entirely on its own books.

Sunday, October 2, 2016

Why are European banks so shaky?

..because it is relatively easy for them to evade minimum capital requirements.

Research by colleague Benjamin Munyan shows that European banks sell their debt on the last day of each quarter, temporarily turning their debt into cash, if only for one day. On the next day, these "repo's" are bought back by the bank, turning their cash back into debt.

This "window dressing" occurs on the day when the European regulators "check" banks' debt/equity ratios. US banks don't have this problem because US regulators check the debt/equity ratios over the entire quarter.

BOTTOM LINE: Such window dressing "...understates a dealer bank’s leverage and maturity mismatch, which means systemic risk is higher than we would believe using only quarter-end measures."

Be careful what you measure.

Research by colleague Benjamin Munyan shows that European banks sell their debt on the last day of each quarter, temporarily turning their debt into cash, if only for one day. On the next day, these "repo's" are bought back by the bank, turning their cash back into debt.

This "window dressing" occurs on the day when the European regulators "check" banks' debt/equity ratios. US banks don't have this problem because US regulators check the debt/equity ratios over the entire quarter.

BOTTOM LINE: Such window dressing "...understates a dealer bank’s leverage and maturity mismatch, which means systemic risk is higher than we would believe using only quarter-end measures."

Be careful what you measure.

Subscribe to:

Posts (Atom)