In the long run, nothing else matters. GDP buys you health, advancement of the disadvantaged, social programs, international security, and climate if you are so inclined. Without GDP, you get less of all. Economic policy should have one central goal -- get productivity growing again, or (in my view) get out of the way of its growth. This is the one little hope that has not been let out of the policy Pandora's box, focused on everything else right now.

Macroeconomists classify two basic types of growth:

- More inputs (labor, capital) lead to more output (GDP)

- Technological progress (Total Factor Productivity) increases output for the same level of input.

Here is a graph of the Total Factor Productivity in the US

And here is the change in Total Factor Productivity across countries.

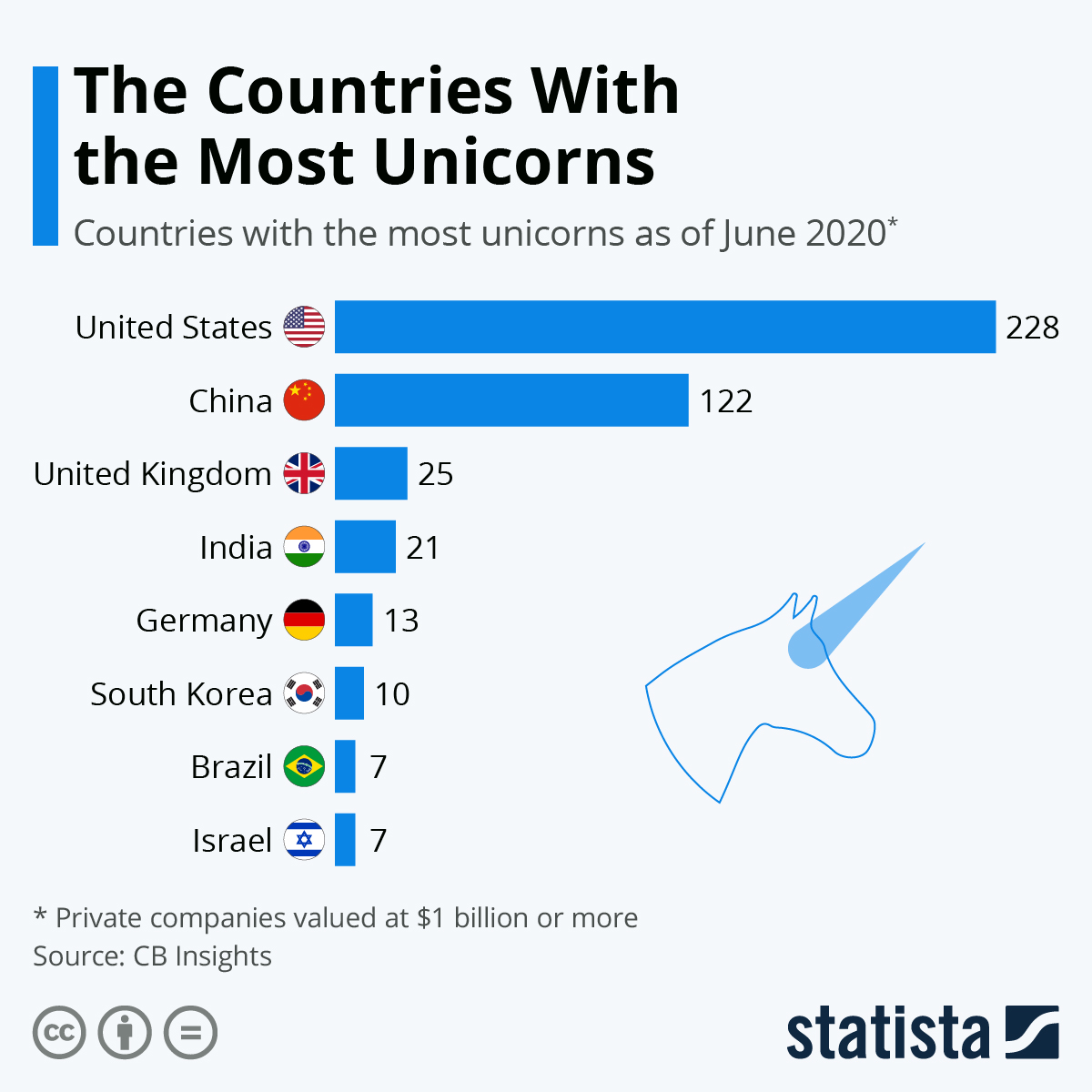

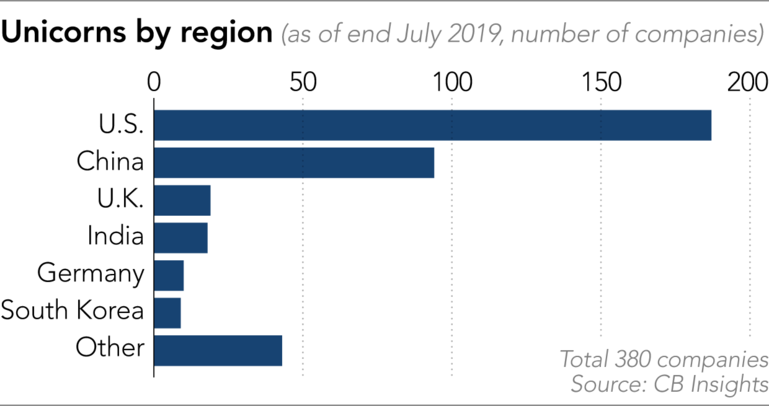

We have blogged about the dearth of unicorns in the EU,

Total Factor Productivity seems to be telling the same story.

{kind=link}

{kind=link}

{kind=link}