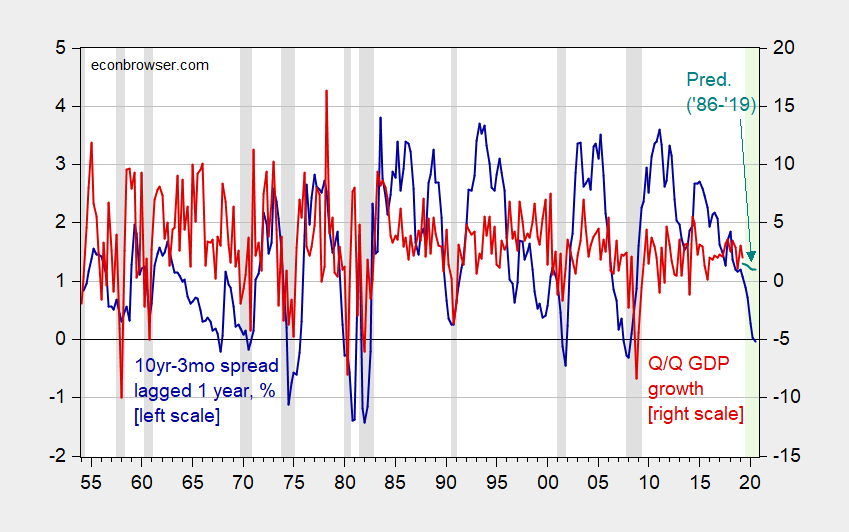

In the graph above, we plot two time series, the percentage growth in GDP (in red) and the difference between long and short term interest rates (in blue). The red series has a mean somewhere between 1% and 2%. The so-called "yield curve" (in blue) is usually positive to account for the greater risk of long term bonds.

In all of past recessions in the graph, when the blue line has dipped close to zero before the red line goes negative. Recently the difference has approached zero, which could be a signal of a coming recession. Here is the theory:

Under unusual circumstances, investors will settle for lower yields associated with low-risk long term debt if they think the economy will enter a recession in the near future. For example, the S&P 500 experienced a dramatic fall in mid 2007, from which it recovered completely by early 2013. Investors who had purchased 10-year Treasuries in 2006 would have received a safe and steady yield until 2015, possibly achieving better returns than those investing in equities during that volatile period.

In other words, (i) if the alternative to holding treasuries is investing in the stock market, and (ii) you expect the stock market to fall in the the short term, then get out of equities into long-term bonds. This drives up the price of long-term bonds. Higher bond prices imply a lower yield because yield=(bond payment)/price.

NOTE: there is one "false positive" for this indicator, in 1967, when the dip in the yield curve did not signal an immediate recession.

DISCLAIMER: If I really knew that a recession were coming, I wouldn't be teaching school, and I probably wouldn't tell you.

I have three ironclad rules of thumb for determining that a recession is nigh.

ReplyDelete1) The yield curve inverts.

2) The Fed starts lowering rates.

3) The "This Time Is Different!!!" people start crawling out of the woodwork to explain why the first two are wrong this time and things are actually going fantastic.

The crucial one is the yield curve. The yield curve doesn't *predict* recessions, it helps *cause* them. Banks make money by "borrowing short and lending long". When the yield curve inverts, bank profits suffer, so they respond by tightening credit, which increases pressure on marginal companies.

I am genuinely curious whether the "This Time Is Different!!!" effect merely represents a bifurcation of thought (some people are pessimists while some are optimists), or is a "conspiracy" used to prop the market long enough for the smart money to find a "greater fool" to sell their stock to.

Claims that "You can't predict a recession!" are both right and wrong. Right, in the sense that you can't tell the hour or the day, or often even which specific event will puncture the economic equilibrium. Wrong, in the sense that you *can* tell when conditions are coming into phase for a recession.

It's similar to the weather. The weather forecaster can't tell me if a tornado is going to hit *my* house, only that conditions are primed for tornadoes *somewhere*. So when I see storm clouds on the horizon, whether atmospheric or economic, it's prudent to go inside until the storms passes.

As all three have come to pass, I rotated my 403b into bonds back in June, when the markets were a lot more optimistic than today.

This is all starting impact my sleep a night and while I could just drink an extra glass of wine I would prefer that there was less uncertainty on where things will be in a year from now.

ReplyDeleteUseful article, thank you for sharing the article!!!

ReplyDeleteWebsite bloggiaidap247.com và website blogcothebanchuabiet.com giúp bạn giải đáp mọi thắc mắc.