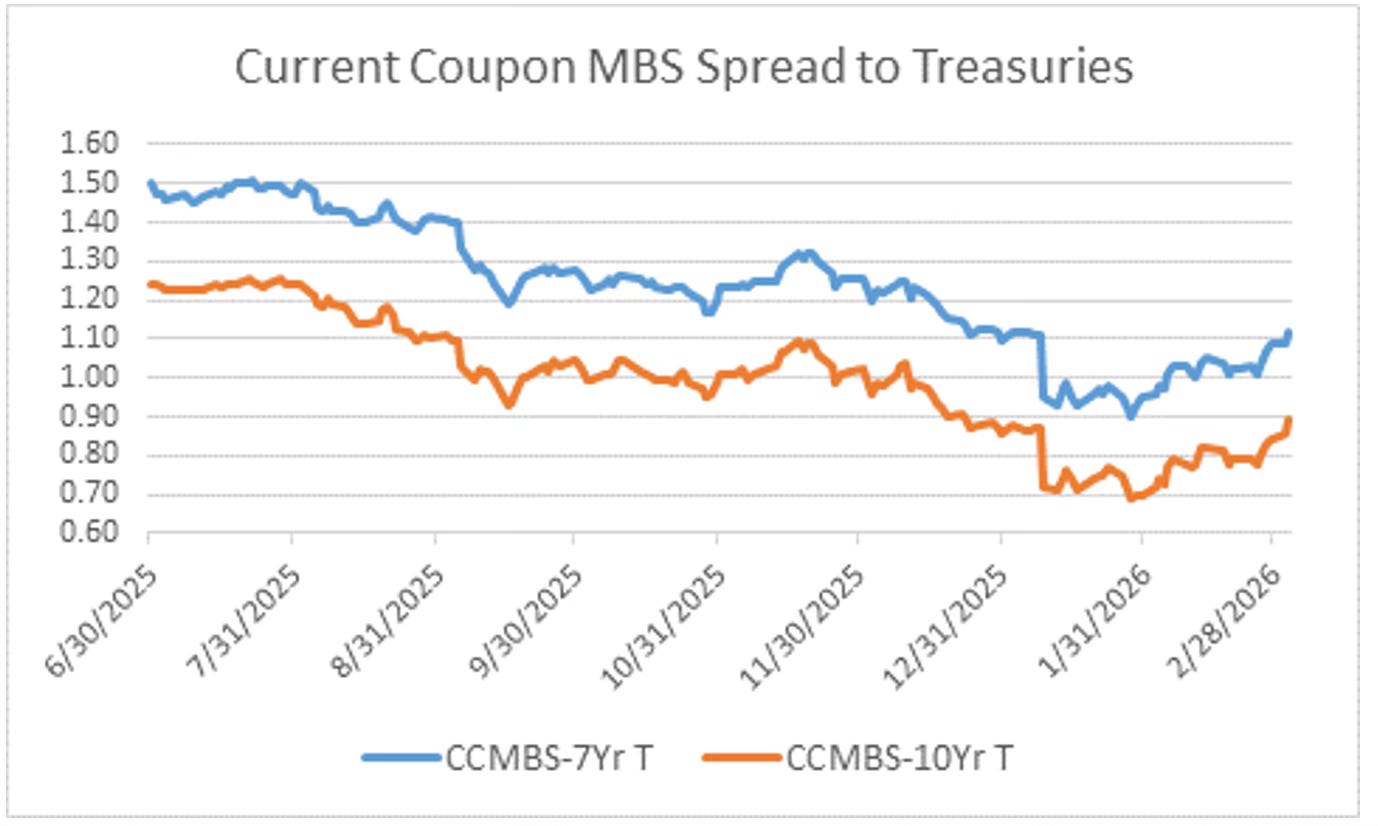

CCMBS/Treasury spreads, in contrast, widened significantly last month

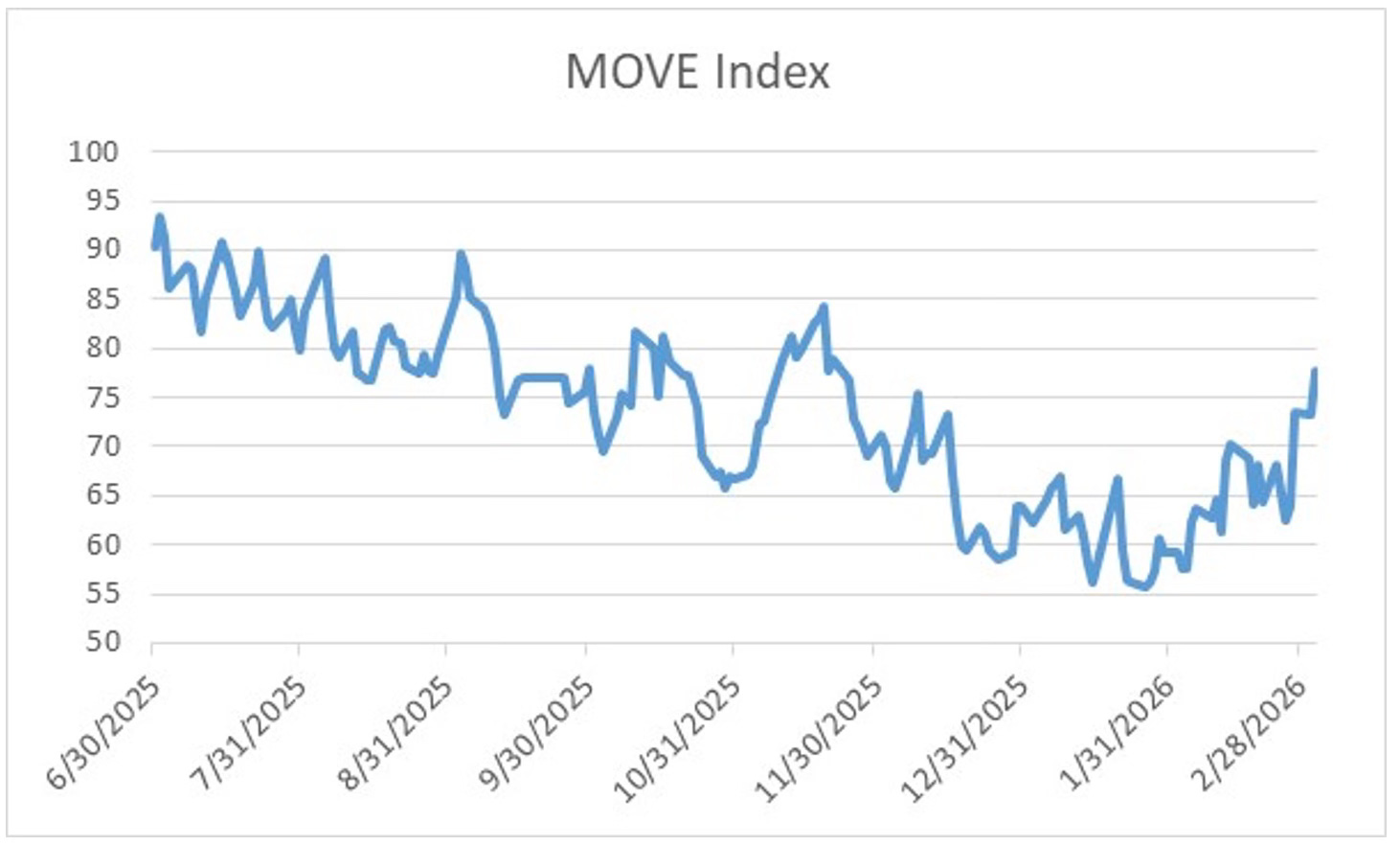

One reason CCMBS/Treasury spreads have widened since January is that implied and actual interest rate volatility [a measure of risk] has increased ... Below is a chart of the MOVE index, a measure of implied interest rate volatility from options on Treasury securities across the curve.

No comments:

Post a Comment